- Types of Insurance Every Subcontractor Should Consider

- Legal and Regulatory Compliance Overview

- Assessing Your Projects’ Risk Profile

- Steps to Evaluate Insurance Providers

- Tips for Comparing Coverage Options

- Cost-Benefit Analysis: Insurance Premiums vs. Risk Mitigation

- Case Studies: Success Stories and Lessons Learned

- Avoiding Common Pitfalls and Lapses in Coverage

- Future Trends in Subcontractor Insurance Requirements

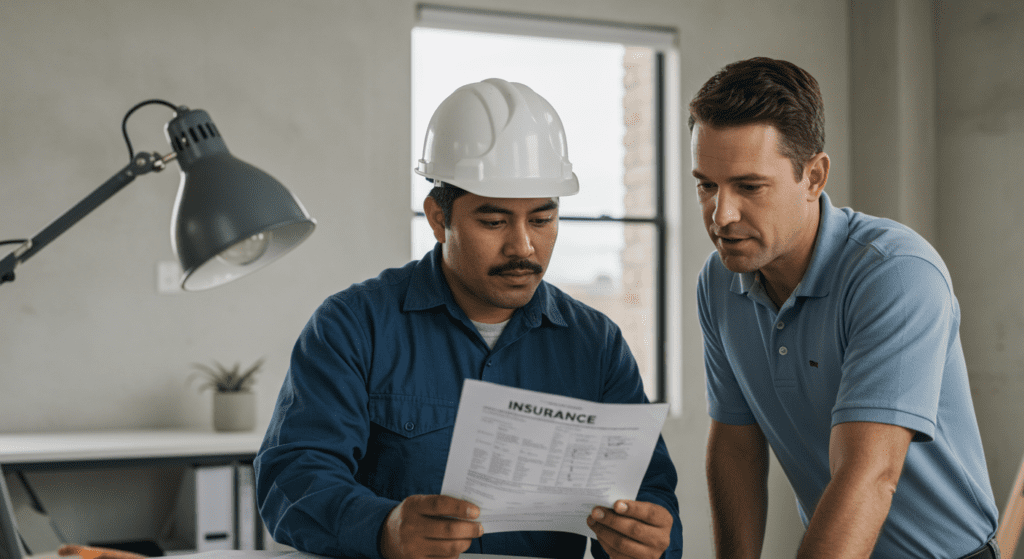

Subcontractor insurance is a crucial investment for anyone in the construction or contracting industry. It not only protects your business from unforeseen incidents, but it also builds trust among project partners and clients. Insurance provides financial security in cases of on-site accidents, property damage, or claims of negligence. For subcontractors, maintaining a comprehensive insurance policy is essential to demonstrate professionalism and compliance with contractual obligations. These safety nets ensure that the potential fallout from unexpected events does not cripple your operations.

1. Types of Insurance Every Subcontractor Should Consider

There are various insurance policies designed to address the unique challenges faced by subcontractors. General liability insurance is often the first line of defense, covering property damage, bodily injury, and legal costs. Professional liability insurance, also known as errors and omissions insurance, protects you against claims arising from poor workmanship or oversight. Workers’ compensation is another vital policy, covering medical expenses and lost wages for employees who suffer injuries on the job. In addition, equipment and tools insurance, inland marine insurance, and auto liability insurance for business vehicles provide a full suite of personalized coverage options. Choosing the right mix can depend on the specific projects, the size of your operation, and the risks associated with your work.

2. Legal and Regulatory Compliance Overview

Subcontractor insurance is not just a safety measure—it is also often a legal requirement. Various state and federal regulations mandate specific types of coverage for workers in the construction industry. Adhering to these regulations helps avoid legal penalties and maintains eligibility for public and private projects. Subcontractors must ensure that their policies meet the minimum standards set by governments and industry associations. Staying compliant may also provide more leverage during the bidding process, as clients favor companies that actively manage risk and prioritize safety. Regular consultations with legal advisers, industry experts, and insurance professionals are recommended to keep abreast of changes in regulatory requirements.

3. Assessing Your Projects’ Risk Profile

Before selecting an insurance policy, it is important to understand your project’s risk profile. Assessing the environment where your work takes place is the first step. Consider the nature of the job, the type of materials used, and the dynamics of the work site. Evaluate potential hazards, areas with historical claims data, and environmental factors that might increase the risk of accidents. Assessing risk also means reflecting on the work practices within your organization—ensuring that safety protocols are in place and that employees are rigorously trained in hazard management. Gathering detailed data not only supports your claim for more tailored insurance coverage but also forms the basis for implementing your internal risk management strategies.

4. Steps to Evaluate Insurance Providers

Choosing the right insurance provider is as critical as selecting the right type of policy. Start by looking for insurers with deep industry experience and a strong reputation among subcontractors. Obtain multiple quotes and compare them on the basis of premium costs, coverage limits, deductibles, and claim resolution processes. Ask for customer feedback and case studies to gauge their efficiency during claim processing. It is also beneficial to investigate the insurer’s financial stability—this is essential for ensuring that they can cover large claims when necessary. Meeting in person with agents can help clarify policy details and tailor the terms to match the specific needs of your projects. A reliable provider should work with you to customize coverage at competitive rates.

5. Tips for Comparing Coverage Options

When comparing insurance policies, clear and careful examination of the policy documents is necessary. Look for any gaps in coverage and clarify ambiguous terms. Ask questions about exclusions and any conditions that might render the policy void in certain circumstances. It is important to evaluate what risks are covered not just in the present but also taking into account future project ventures. Use a side-by-side comparison tool to list features such as liability limits, types of coverage included, and deductibles. Pay attention to the process for filing and resolving claims. In many cases, a slightly higher premium may be warranted if the provider has a swift and effective claim settlement history. This proactive approach helps you secure policies that align with your needs and project demands.

6. Cost-Benefit Analysis: Insurance Premiums vs. Risk Mitigation

The primary purpose of subcontractor insurance is risk mitigation. While premiums can add significant overhead to project costs, the cost of inadequate insurance can be far higher. A thorough cost-benefit analysis involves understanding the potential financial impact of accidents, lawsuits, or business interruptions against the routine cost of maintaining insurance. Attach a tangible value to the peace of mind provided by robust policies. In many ways, good insurance acts as a safety net that can prevent the collapse of a business after a single major incident. Such analysis can also expose areas where investing in additional risk management measures could lead to lower premiums in future policy renewals, making your overall operation more financially resilient.

7. Case Studies: Success Stories and Lessons Learned

There are many stories in the industry that underline the importance of comprehensive subcontractor insurance. In one case, a subcontractor experienced a severe equipment accident that risked spiraling liabilities. Thanks to sufficiently comprehensive equipment and casualty coverage, the business was able to cover repair costs and legal fees without significant financial strain. In another instance, a small construction firm successfully defended a claim related to alleged professional negligence because it had invested in errors and omissions insurance. However, some lessons come from instances where lapses in coverage led to crippling lawsuits or project shutdowns. These case studies prove that thorough analysis and appropriate insurance coverage can mean the difference between business continuity and financial disaster.

8. Avoiding Common Pitfalls and Lapses in Coverage

Common pitfalls include cutting corners to minimize expenses by opting for bare-minimum coverage. Such decisions can backfire when claims exceed limits or when certain areas of risk are not adequately covered. Another risk involves failing to update policies as the business evolves. As projects vary in scope and geographic location, static coverage plans quickly become obsolete. Additionally, some subcontractors overlook the importance of reading the fine print or fail to understand complex policy terms. Keeping close communication with your insurance provider and periodic reviews of the policy terms can prevent lapses in coverage. Stability and flexibility in your insurance arrangements allow you to adjust your coverages in line with unforeseen challenges and evolving market standards.

9. Future Trends in Subcontractor Insurance Requirements

The landscape of subcontractor insurance is evolving rapidly. Future trends indicate an increased emphasis on digital risk management that involves the integration of smart technology for real-time safety monitoring. Insurers are looking into incorporating data on on-site behavior and safety practices to shape dynamic premium models. Increasingly, you may find that policies are tailored to specific project types and risk categories rather than blanket covers. Legal updates and environmental concerns are also influencing policy structures, pushing for more comprehensive coverage in scenarios involving regulatory or environmental challenges. Staying informed about developments like cyber liability—which covers risks of data breaches affecting project operations—is crucial as technology continues to change working environments. Embracing these trends means preparing for an era where risk checks and dynamic adjustments become the industry standard.

Conclusion

In conclusion, subcontractor insurance stands as a cornerstone of risk management in the contracting industry. By understanding its importance, assessing your risk profile, and choosing the right providers and policies, subcontractors can safeguard their operations while meeting legal obligations. Through careful evaluation and periodic policy updates, you can balance the costs of premiums with the invaluable benefits of risk mitigation. The evolving landscape, combined with lessons from past experiences and success stories, shapes a more resilient and compliant future for subcontracting businesses. As regulations tighten and projects become more complex, each subcontractor must approach insurance as a continuous investment rather than a one-time purchase—a strategic asset that protects both your financial health and professional reputation.